State of Crypto Credit Markets (Dec 2022)

The need for credit infrastucture to evolve

In this article, I will delve into the State of Crypto Credit market, focusing on four specific credit verticals:

CeFi Credit

DeFi Credit (undercollateralized & overcollateralized)

TradFi Credit

Real World Asset ("RWA") Lending

By analyzing these credit sectors, I aim to provide a comprehensive overview of the current landscape of crypto credit and offer insights into why I think crypto credit needs to evolve.

CeFi Credit

Lending activity amongst centralized lenders continues to be at a standstill. While large lenders like BlockFi have already filed for Chapter 11, the full extent of contagion from FTX/Alameda saga remains yet to be known.

Genesis Trading, the lending subsidiary of Digital Currency Group (DCG), has yet to reveal any solution for its liquidity crunch since it halted withdrawals on Nov 16 – this remains the largest overhang in crypto credit.

It will take time for new credit to be issued, probably mid-Jan 2023 at the earliest once borrowers’ quarterly and year-end financials are refreshed and reassessed, and once there is further clarity on next steps for Genesis.

DeFi Credit (undercollateralized)

Unless already in default, borrowers on undercollateralized DeFi lending pools have fully repaid all loans (evident in TVL decline). Remainder TVL represents assets sitting idle in pools with 0% utilization (excluding RWA-based lending protocols, more on this later).

There were two notable events in the past month (both related to FTX exposure)

Orthogonal Trading’s $36M loan default (30% of active loans on Maple)

Auros’ 2,400 wETH missed principal payment (pending resolution)

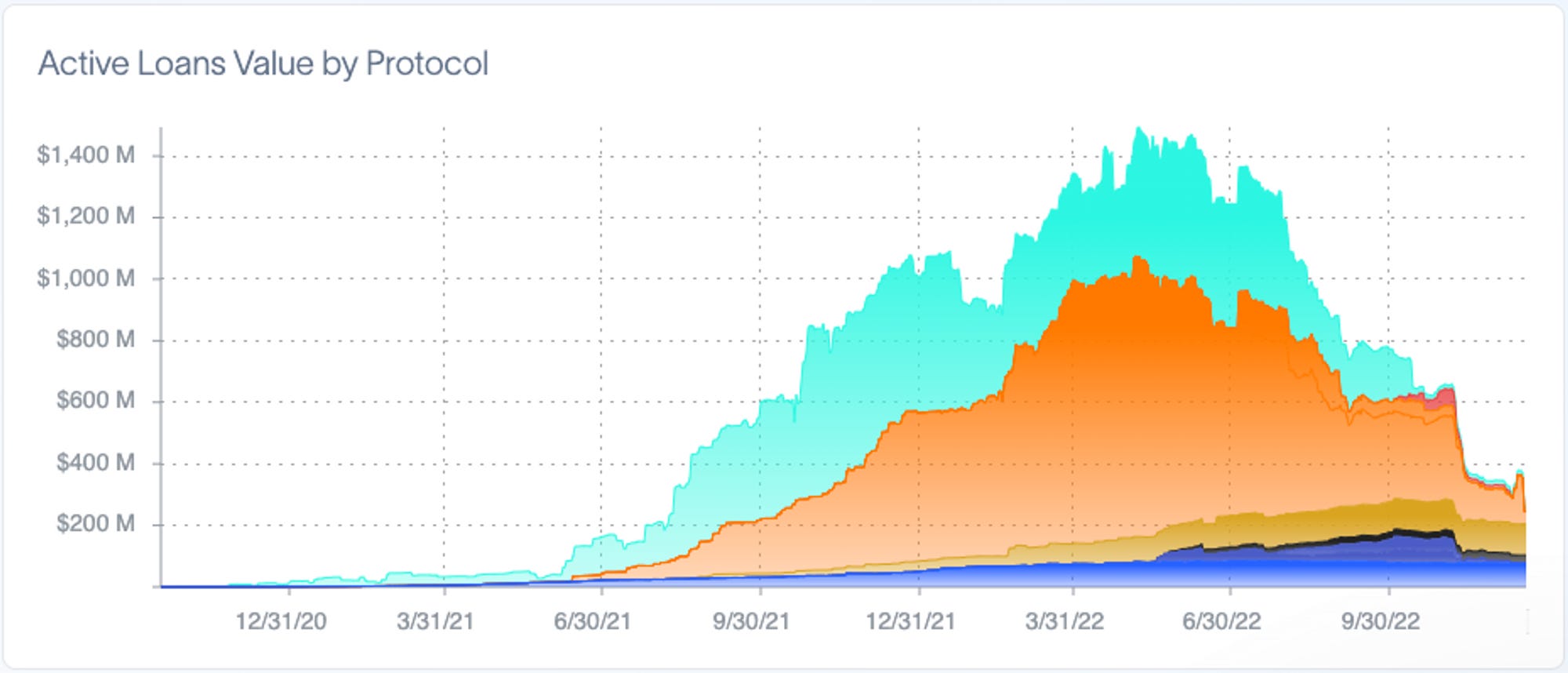

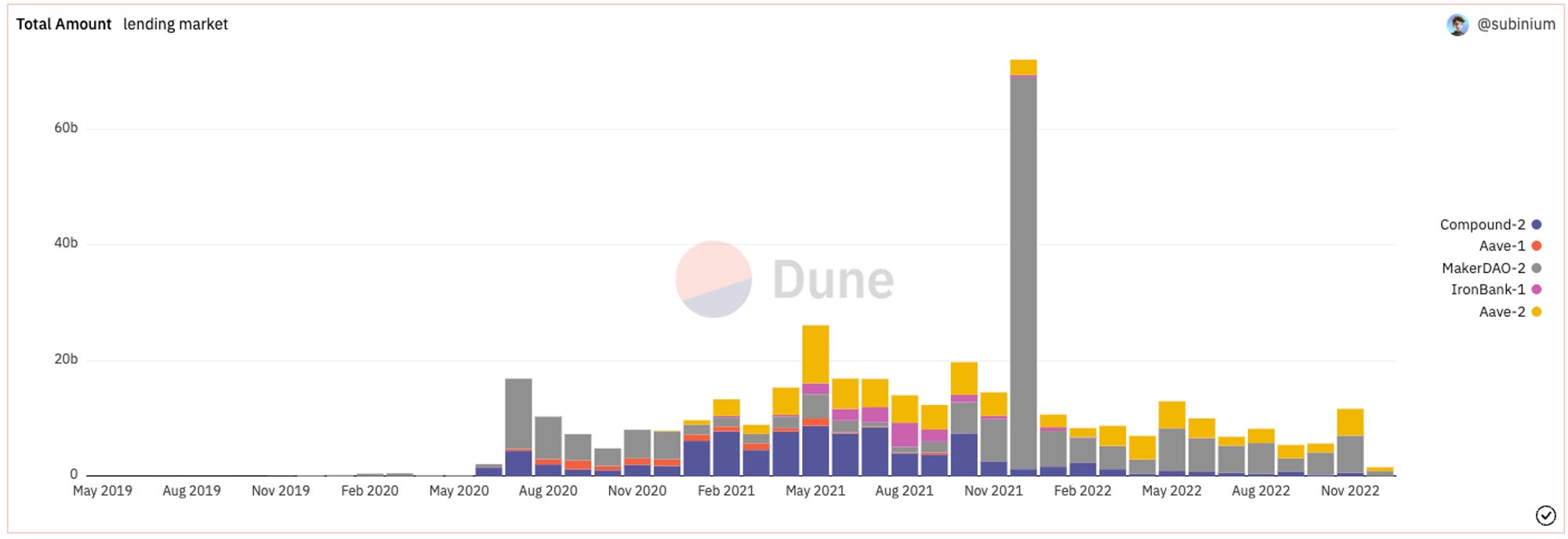

DeFi Credit (overcollateralized)

Total DeFi lending markets are at levels not seen since end-2020 (pre-bull market).

Additionally, both Aave and Compound (top 2 largest lending markets for USDC) have passed proposals to freeze/cap borrow liquidity (mainly on long-tail assets) out of abundance of caution during this risk-off period.

TradFi Credit - Crypto Debt

Investors remain risk-off any debt that is related to crypto – with COIN and MSTR bonds trading at 49/51c on dollar (13/24% last traded yield) respectively.

TradFi Credit - US Treasurys

Since early Nov 2022 (pre-FTX crunch), the long end of the curve has come down, while the short-end (3mo) remains elevated.

Visibly further yield curve inversion.

Real World Asset ("RWA") Lending

While crypto credit and macro conditions may appear bleak, it is worth noting that crypto credit has only been around for <6 years – 2016: BitMEX invented the world’s first perpetual swap product on XBTUSD; 2018: Genesis started their lending business and Compound launched money markets on Ethereum.

Additionally, up till 2022, crypto lending has been largely circular i.e. barely any connection to the real world.

RWA lending bridges assets and yields between crypto and traditional markets, i.e. private credit, bonds, Treasurys etc available on-chain in crypto.

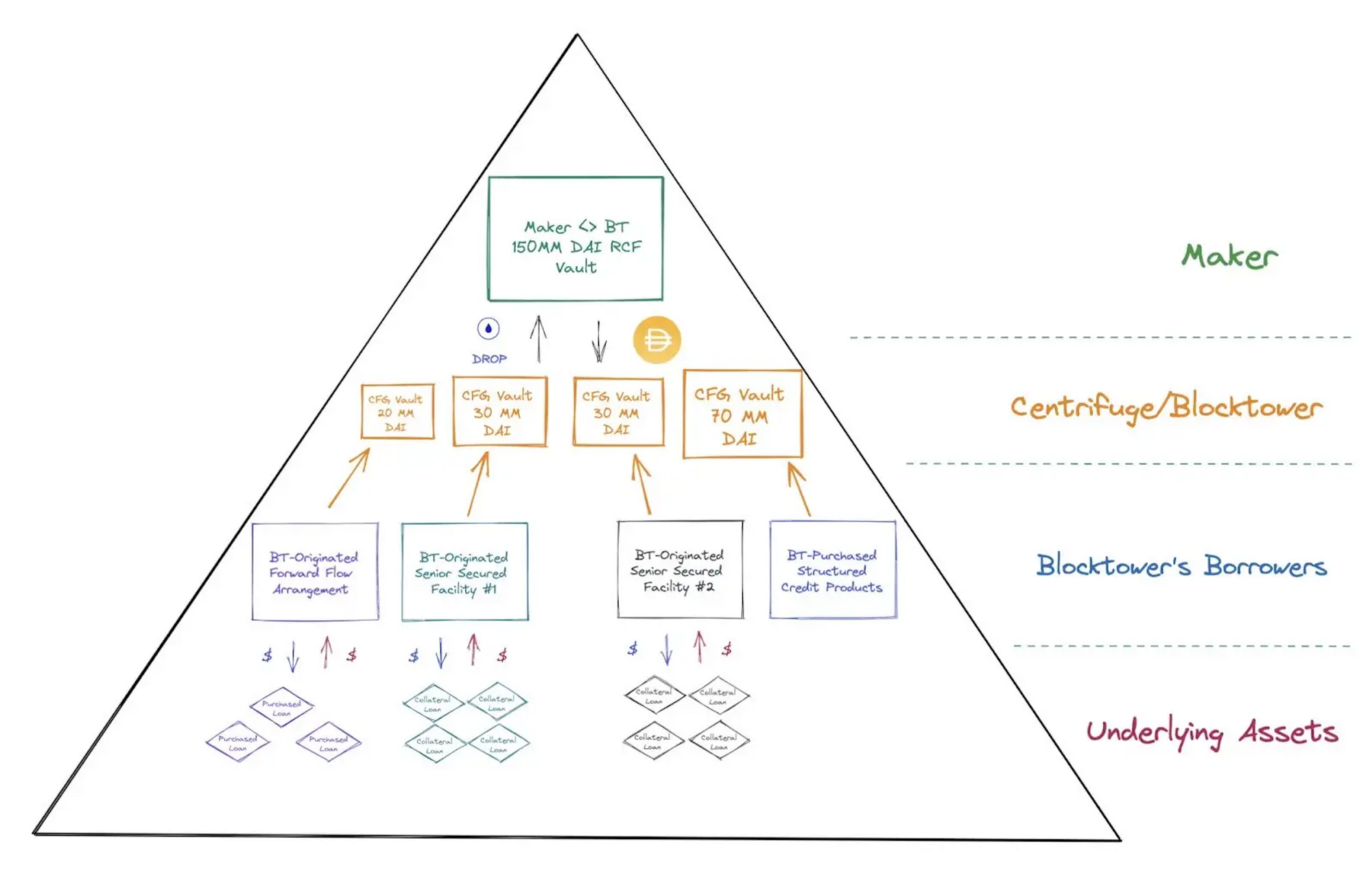

On 11 Dec 2022, amidst this crypto deleveraging period, an Executive Proposal was passed to introduce multiple RWA Credit Vaults run by BlockTower on Maker.

BlockTower is borrowing $150M from DeFi to invest in real world loans to fintechs/non-banks.

Akin to CLOs, Maker will deploy vaults for BlockTower's structured credit investment:

Tranches: 30% BlockTower Junior ($70M) / 70% Maker Senior ($150M; across 4 RWA pools)

Senior @ 4% pa

60-month term

collateralized by short term credit (1-3 year loans to fintechs/non-banks)

It is important to note that most of Maker's historical revenues were from ETH and wBTC related flows.

With this development, Maker seems to be doubling down on its growing revenues from RWA lending, which has just crossed >50% of Maker's revenue as of end-Nov.

Market Thoughts

Ironically, this could be the reset we need in crypto credit. Perhaps even a rite of passage for an emerging asset class.

Crypto has only been through one credit cycle, i.e. this is the first time crypto credit has been truly battle-tested since 2018. Traditional markets, on the other hand, have been through at least 48 debt crises in history.

Perhaps the market needs to move away from speculative & circular lending within a closed ecosystem at very short durations, to structured credit with longer fixed terms at fixed rates and proper tranching – with on-chain transparency.

To a system which facilitates thoughtful and structured credit creation. A system that marries structure and creditor protection in traditional credit markets, with the transparency and composability of DeFi.

Resulting in a completely novel solution.

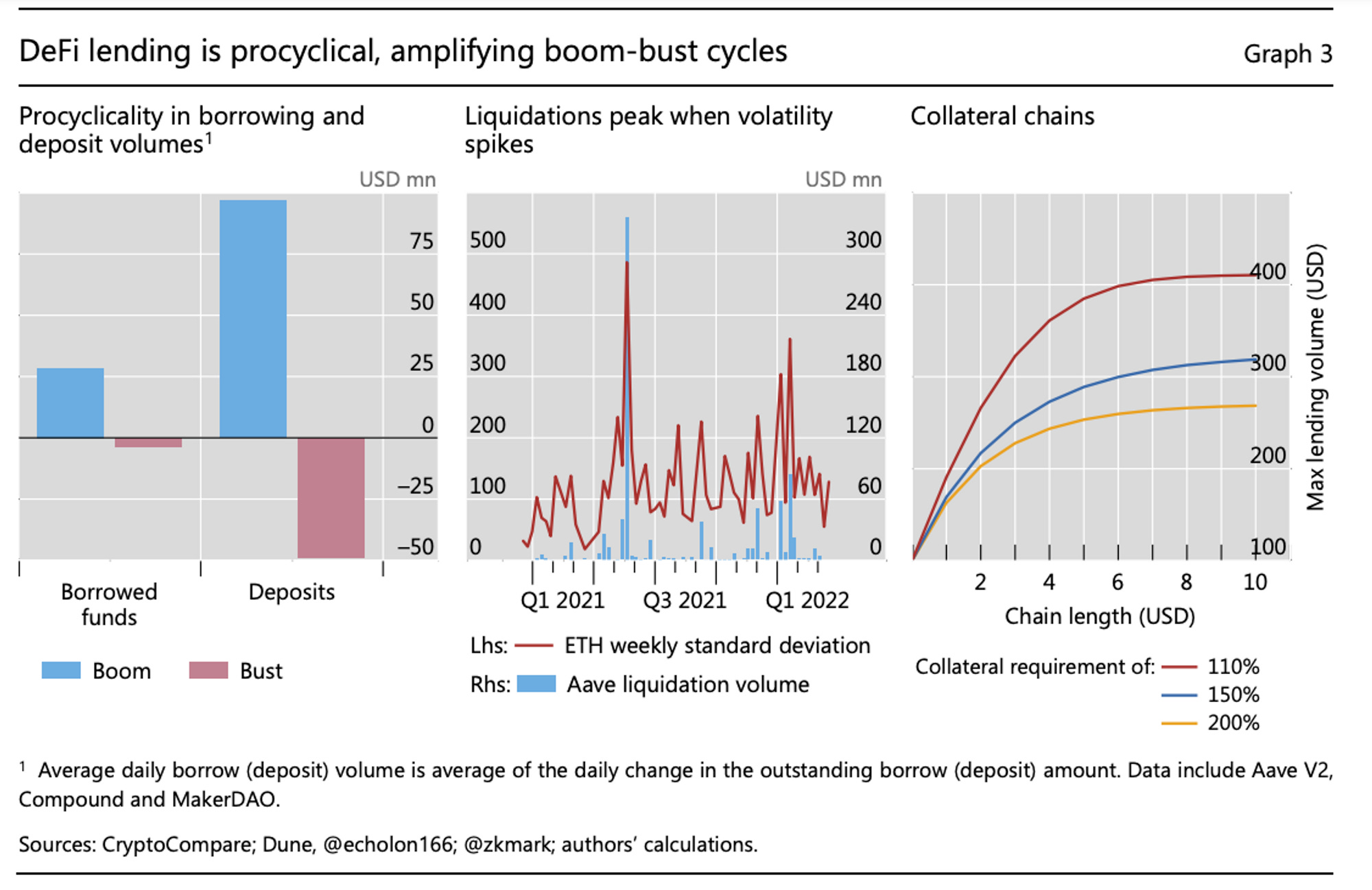

In this cycle, we have clearly proven the demand for crypto credit, albeit still at a very nascent stage:

Lending/borrowing activities have been largely speculative in nature

Circular reliance on coin collateral leads to procyclicality (chart below)

No risk-free rate

No tradable debt markets

Crypto credit clearly needs diversified collateral and reference rates (coins -> RWAs), structured credit (open -> fixed term), and institutional DeFi infrastructure to facilitate more of these flows.

The thesis remains stronger than ever – there is no time like a bear market to build breakthroughs.

Nothing written on ken-chia.com is financial advice.