Crypto Financialization & The Yearn For Yield

(5 min read)

This week's issue of Bridging Bitcoin can be read in 5 mins and 12 seconds.

Have feedback on Bridging Bitcoin, or have any topic requests? Send it our way to ken.chia@substack.com.

For those who are not yet subscribed, I write on Bitcoin and cryptocurrencies from a macro perspective. If that interests you, subscribe to get a weekly issue delivered directly to your inbox:

Top developments:

MassMutual Joins the Bitcoin Club With $100 Million Purchase (WSJ). Massachusetts Mutual has become the first life insurance company to publicly announce that they have purchased $100m of Bitcoin as part of their investment strategy. Insurance companies are generally the most conservative of investors, so this could be seen as a huge step for institutional adoption.

One River Asset Management has emerged as one of the largest investors in Bitcoin after quietly buying more than $600 million in cryptocurrencies. The hedge fund has commitments that will bring its holdings of Bitcoin and Ether to about $1 billion as of early 2021 (Bloomberg).

Coinbase, the largest cryptocurrency exchange in the U.S. files for IPO. Oh, and in case you really missed it, Bitcoin is above $23,000 at time of writing (CNBC).

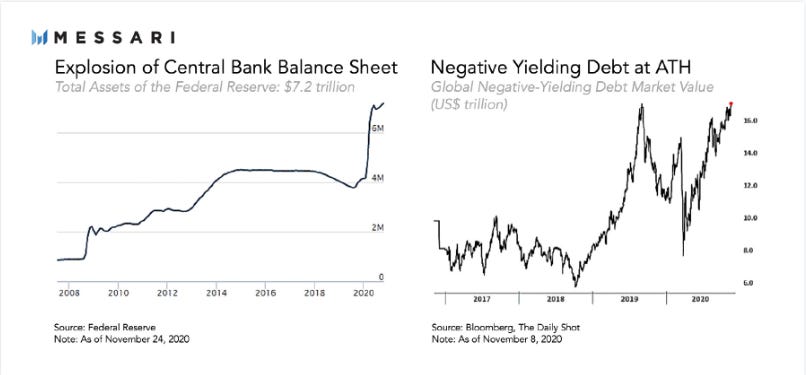

The Global Yield Environment

We live in an environment where interest rates in the developed world are at or below zero. In the yearn for yield, funds flock towards equity markets which are propped up above the never-ending cloud of fiscal economic stimuli – in 2020, despite being in a global pandemic-driven recession, the S&P 500 posted 31 new 52-week highs and no new lows. Central bank assets and negative yielding debt are both at all time highs, raising questions on whether central authorities have any more monetary levers to pull.

Source: Messari

Despite a low interest rate environment, which should incentivize more borrowing, the global lending market is expected to decline due to the economic impacts of COVID-19.

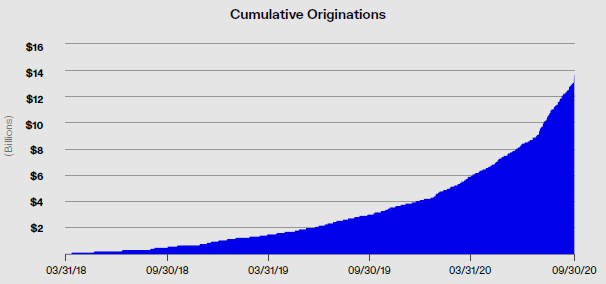

The one bright spot in the lending market is crypto lending. Genesis, the world's largest digital asset lender, has more than doubled its new loans from the previous quarter to a record $5.2B in loan originations.

Wait - why would people borrow and lend against something so volatile like Bitcoin?

In banks and lending businesses, loan collateral assets serve as a form of security to loans, minimizing risks for lenders. All things held equal, lenders would prefer collateral assets that are liquid and relatively stable in value.

And while even the likes of Ray Dalio believe that Bitcoin has now established itself as a "gold-like asset alternative", its price action and correlation to risky assets maintain its existing status as a highly speculative asset.

So why would people borrow and lend against Bitcoin?

The Bitcoin Lending Market

From a US person's perspective, common financial milestones in life include buying a home, or (arguably even more rewarding) paying off your student debt.

Let's use John, an American millennial in his 30s, to illustrate. John is a long time Bitcoin HODLer since he bought 20 bitcoins in 2014 @ $500 per piece (don't we all wish?).

Since his holdings have 40x-ed in value (fist pump), John decides to buy a new home, settling down with his wife as newlyweds. But, if John were to fund the down payment with his (read: massive) Bitcoin gains, he would have to take an almost equally massive hit in the form of capital gains tax.

Taxman: Do not pass Go, do not collect $200... just, don't.

Borrowing. Today, there are services that allow John to borrow a loan in dollars to fund his expenses, collateralized by his Bitcoin holdings without having to sell. And, if John decides to forgo that home purchase, and instead use that liquidity to make other investments, not only would he not have to pay those taxes, he could also deduct the interest charged on that loan from other capital gains in that same tax year.

Lending. On flip slide to borrowing, John can also lend his Bitcoin to guys like Genesis for yield in return. Since John is a die-hard Bitcoin HODLer (go John!), lending his Bitcoin for yield means he may even never have to sell, since he can live off his Bitcoin interest earnings, especially with current rates of up to 6% p.a. and no fixed lock-up periods.

Players like Genesis borrow and lend to many participants in market like John – both individuals and (more importantly) institutions such as prime brokerage type clients. Genesis, a common bellwether for the crypto lending market, has recorded a whopping $13.6B in total loan originations since its the launch of its lending business in Mar 2018, just over two years ago.

Source: Genesis Q3 2020 - Digital Asset Market Report

Did You Say 6% p.a.?

If you have made it this far, you are probably wondering how in the world are yields so attractive in crypto? Seemingly too good to be true, surely this must be a short-term play if not a potential Ponzi?

The truth is the complete opposite - the crypto yield market is actually extremely attractive with incredibly low risks.

Crypto loans are often conservatively over-collateralized (i.e. 50% LTV) with margin maintenance safeguards in place (72 hours grace period to post additional collateral, in event of margin call). Not intended at shilling BlockFi (one of the largest players in the space), but they explain how this works really well here.

So how are crypto yields so attractive? The crypto yield market is a high growth sector. Yields are high not because it is more risky, but rather because there is less infrastructure (for now). There are also less traditional financial firms that make markets and drive spreads tighter on the playing field (also for now).

Yields and costs to borrow will trend downwards over time. Albeit, we do have a long ways to go before we see crypto yields get close to risk-free rates in the traditional world.

But that's not all: Crypto Financialization

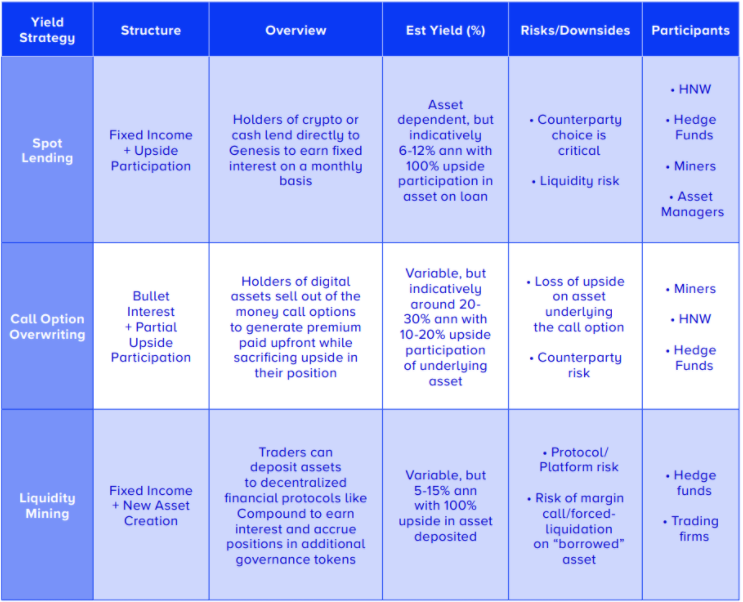

The crypto lending market, while being the largest and most common, is not the only yield-generating mechanism in crypto. Similar to traditional markets, the crypto futures and options markets are some of the others ways to generate (synthetic) yield.

Source: Genesis Market Observations Report Q2 | 2020

There is also liquidity mining, a strategy specific to decentralized finance (DeFi). While I will not be going into technicalities, what I will say is that when looking at yield generation, there are different tranches of risk and return. You can earn more yield but at very different risk profiles.

The main takeaway is that there is a (growing) multitude of yield-generating mechanisms for crypto: some familiar to incumbents in traditional finance, and some specific to decentralized innovations in crypto.

“Yield Get it Eventually…”

Ok, I’ll admit that was a horrible pun…

Crypto yield as a topic is both very broad and very deep – one that I find absolutely fascinating. Since it is impossible to cover everything at one go, what you will take away by this point is this: the crypto lending, derivatives and yield markets are growing at breakneck speeds. Industry players today consist of both former financial veterans and tech pioneers, replicating past innovations in traditional finance (futures, options) while inventing new ones that focus on absolute capital efficiency (DeFi, liquidity mining).

While global rates are at historical lows, crypto players continue to build, resulting in lending and yield rails that are more and more robust, and setting the necessary infrastructure in place for the future of the crypto yield market.

Disclaimer: Nothing written in this post is intended to serve as financial advice. Do your own research.

Have feedback on Bridging Bitcoin, or have any topic requests? Send it our way to ken.chia@substack.com, or

Let’s get in touch. Follow @iamkenchia for real-time musings, and connect with me on LinkedIn.